BNPL software

for businesses & banks

Whether you run a pure-play BNPL service, a merchant-branded instalment programme, or embedded checkout finance, one configurable engine powers pay-in-4, deferred billing, longer instalments, and B2B plans.

Book a demo

Buy Now Pay Later software

for the complete customer journey

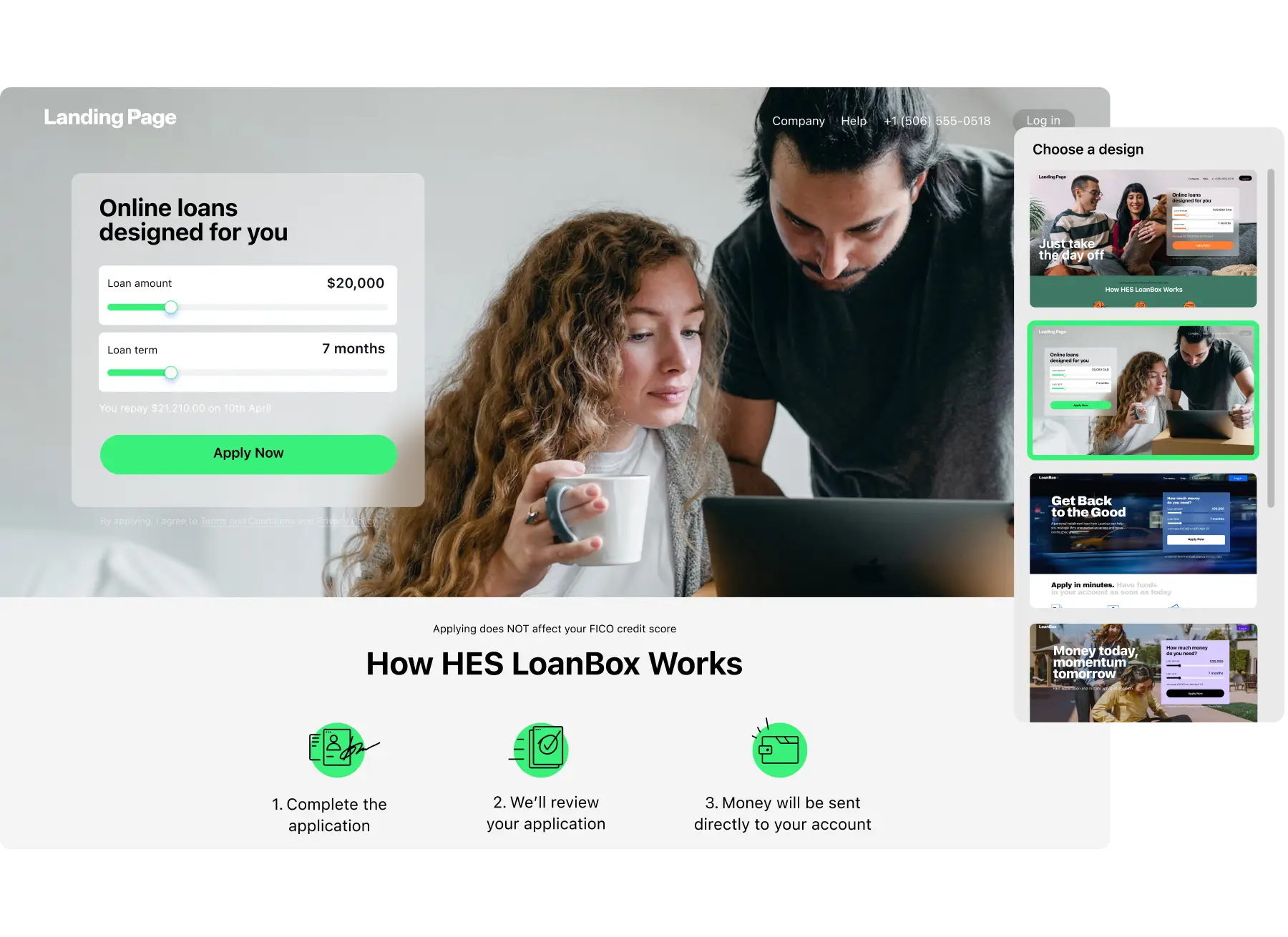

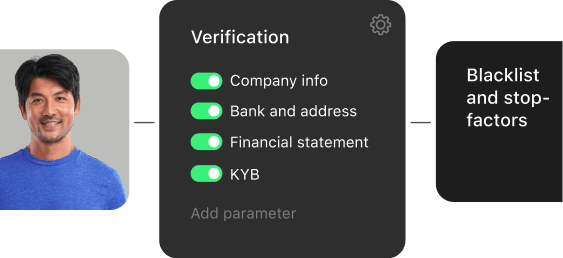

Instant onboarding

Deploy a white-label BNPL software that runs under your brand across web and mobile. Give shoppers a frictionless way to split payments, review terms, and confirm identity in seconds — all in your UI, your colors, your domain. Built on real-time KYC checks, automated decisioning, and seamless merchant integration.

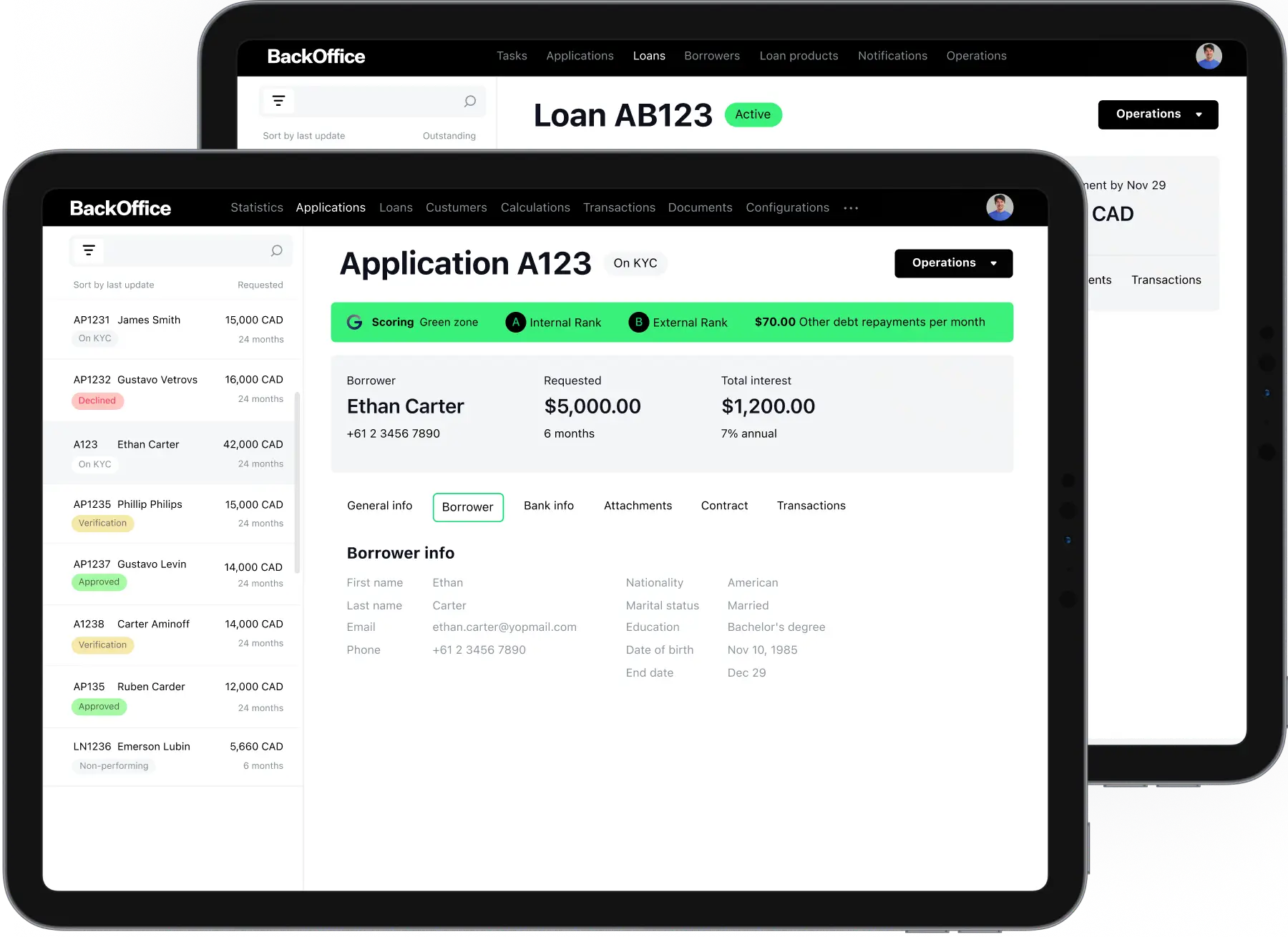

Accurate origination

Approve more customers with confidence using rule-based underwriting, real-time AI scoring, and live data enrichment. Create and manage BNPL plans with merchant-specific eligibility rules, promotional pricing structures, and granular risk controls.

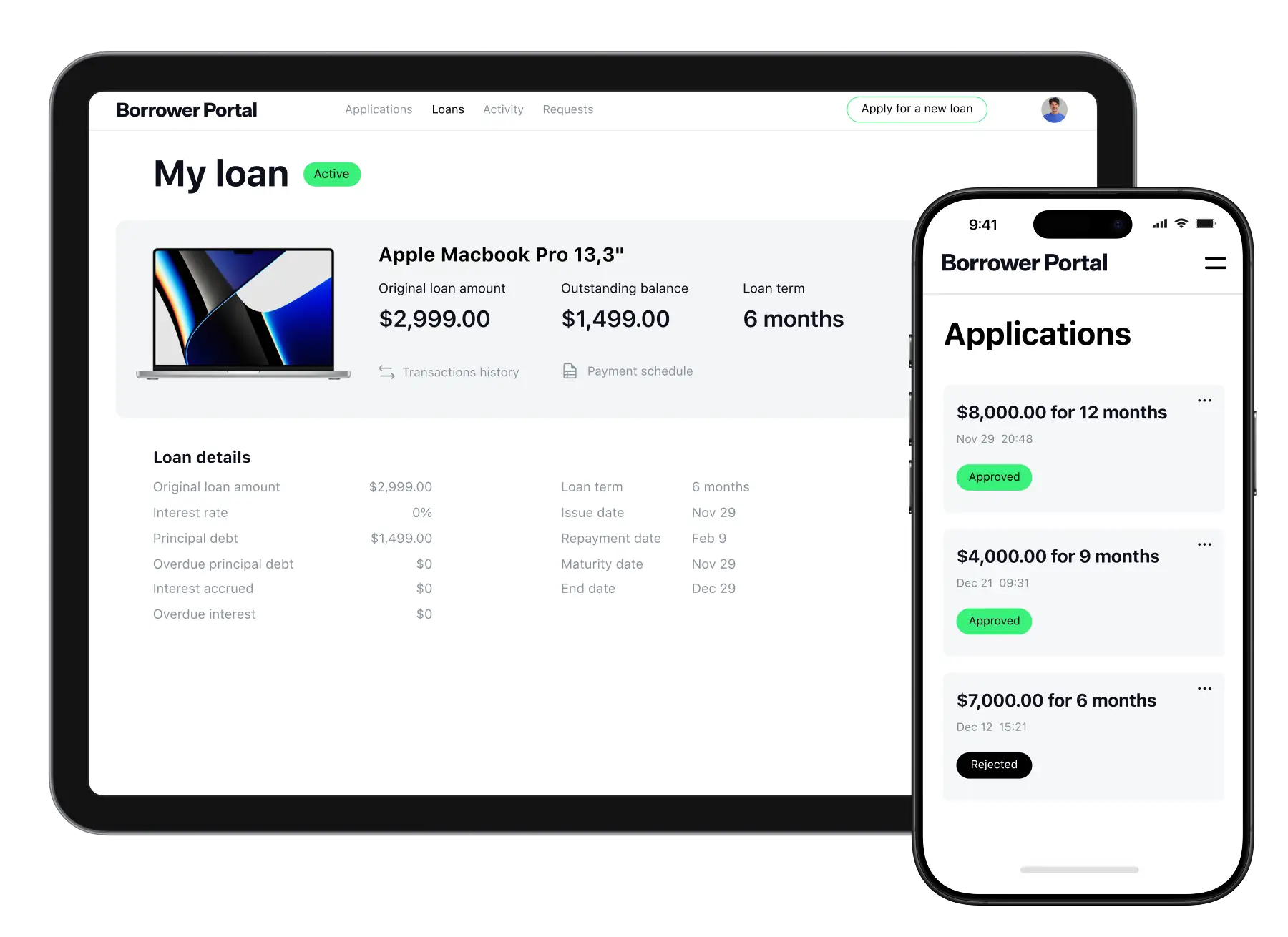

Streamlined servicing

Administer instalment schedules, payment retries, and buyer communications from a centralised workspace. Maintain full transparency across your BNPL portfolio with live repayment tracking and automated customer notifications.

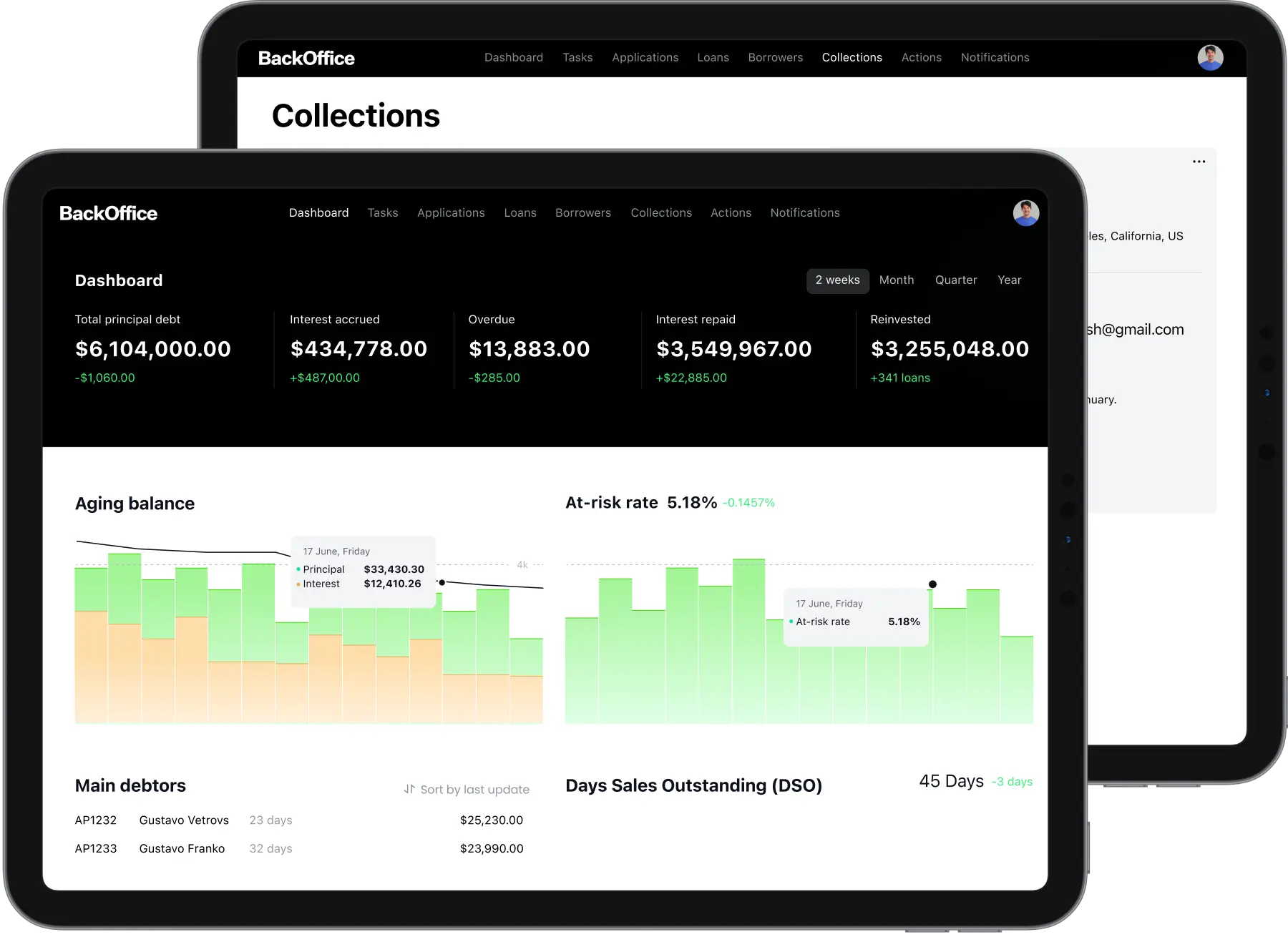

Proactive collection

Recover outstanding balances more effectively with behaviour-based payment reminders, early-stage risk signals, and adaptive repayment options that reduce friction and protect the customer relationship.

Digital onboarding

White-label BNPL that turns intent

into approved purchases

Turn shoppers into approved buyers without losing them between cart and confirmation. Give consumers a fast, transparent path to instalment payments, and give your team the automation to clear high volumes without manual review.

Hold attention from the product page onwards

Decide in seconds without losing the sale

Bring buyers back instead of chasing them

Scale through merchant and partner networks

Loan origination

Cut BNPL origination

time

with AI and

automation

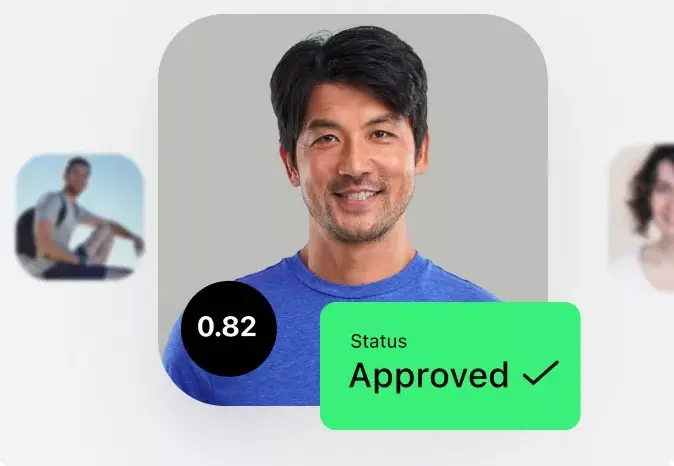

Stalled checks and patchy first-time data quietly bleed conversion and inflate first-payment defaults. AI-driven verification and underwriting turn every Buy Now Pay Later application into a fast, confident, compliant approval before the buyer clicks away.

Instant identity verification and buyer profiling

Configurable underwriting at any speed

AI credit decisioning that grows the basket

Self-learning scoring by GiniMachine

Paperless from cart to confirmation

and much more

Unlimited product configuration

Spin up any BNPL plan your roadmap calls for: pay-in-3, pay-in-4, pay-in-30, six- to thirty-six-month instalments, interest-bearing or zero-interest, B2B trade credit. Configure rates, late fees, merchant-funded discounts, and eligibility per category, market, or campaign without touching code.

Automated contract generation

The credit agreement and pre-contractual information sheet a BNPL purchase needs assemble from your templates as the shopper waits. Per-market wording switches by jurisdiction, so the same checkout serves the UK, EU, and APAC without manual edits.

Smart notification templates

Push, email, SMS, and in-merchant templates fire on events buyers care about: approval, due date, paid-off, dispute resolved. Variables pull live plan data so messages stay accurate after a refund or schedule change.

Role-based security and access control

Shopper data, merchant records, and partner-portal access each sit behind their own permission scope, two-factor sign-in, and device-level controls. Every action gets logged for the audit trail.

Multichannel borrower communication

Reach buyers, merchants, and partners across SMS, email, in-app, and merchant portals with triggers tied to plan status, settlement events, and disputes. Support gets fewer "where is my refund" tickets because the system told everyone first.

No-code workflow builder

Draw BNPL approval paths, fraud branches, and settlement steps on a visual canvas, no developer in the loop. Push changes the morning after a category turns risky and ship new flows in days, not quarters.

Configurable BNPL workflows

Get your lending

product estimate

in 3 minutes

STEP:

/

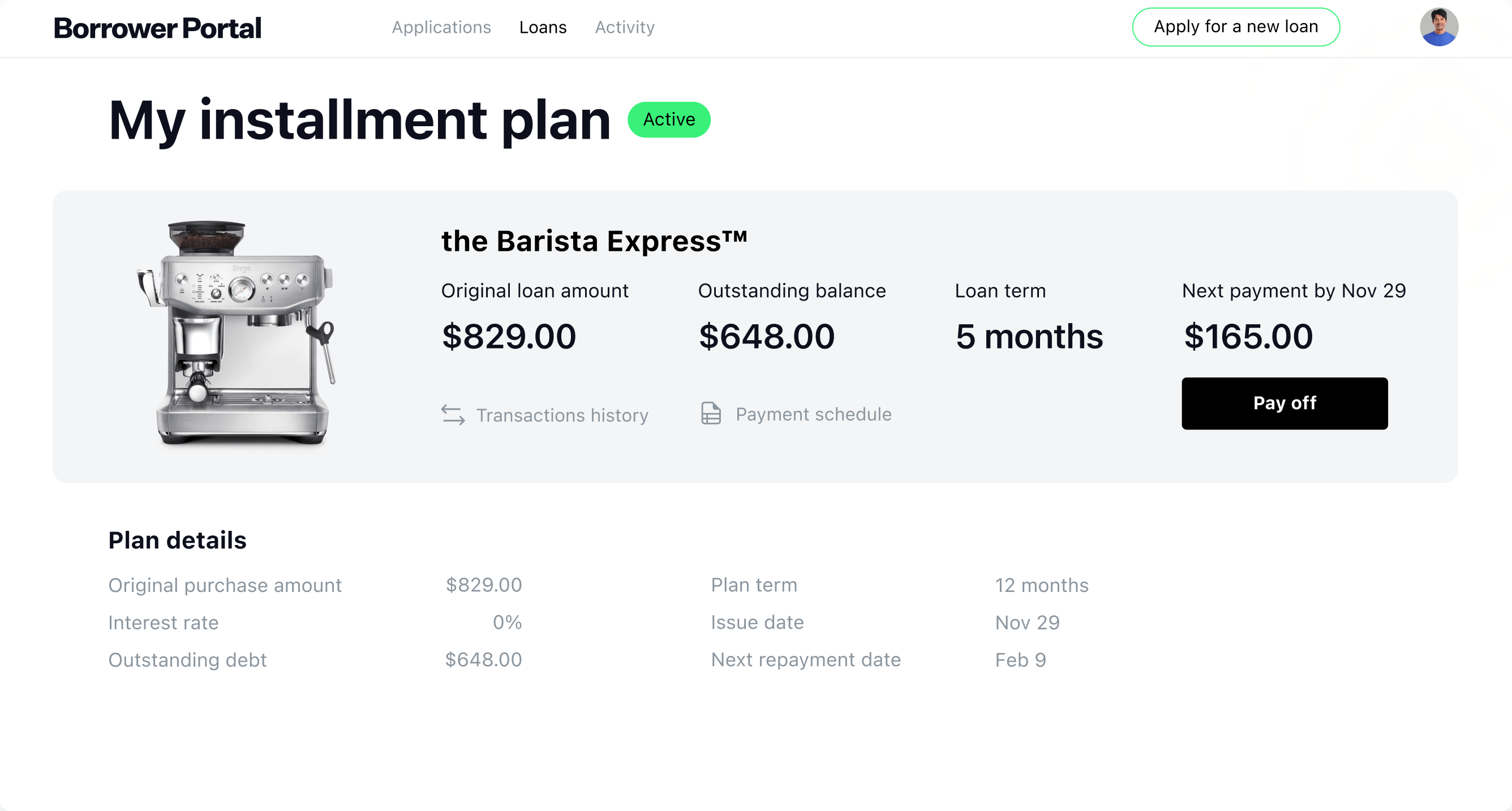

BNPL servicing

Complete Buy Now Pay Later servicing software

Spreadsheets, half-connected ledgers, and merchant settlement files in inboxes quietly drain margin out of every plan. Run BNPL servicing on a single live ledger with flexible terms, automated retries, and pre-integrated payment rails.

Loan lifecycle automation

Comprehensive loan management

360° customer management (CRM)

Trusted payment operations

Drive profit

The platform analyzes borrower data in real time, predicts creditworthiness with up to 3.5x higher decision accuracy, and helps lenders automate decision-making while improving portfolio quality, approval speed, and customer experience.

Real-time AI credit scoring

Personalized lending offers

Portfolio analytics and predictive insights

One space for all details

BNPL collections

Boost recovery on overdue

BNPL instalments

Late instalments on small tickets cost more to chase than they recover, and aggressive dunning sends shoppers to the next BNPL provider. Automate outreach, scoring, and fees with AI that picks who to contact, when, and how.

Automate the full recovery workflow

Tailor every recovery action with AI

Prevent missed payments before they happen

Penalty management built for compliance

100+ integrations to plug into

every BNPL checkout flow

HES LoanBox connects to the stack a BNPL programme runs on: payment processors, card networks, e-commerce platforms, fraud and identity providers, credit bureaus, and open banking, with pre-built integrations and open APIs for anything custom.

BNPL reporting and analytics

HES LoanBox builds interactive dashboards around the BNPL numbers your team actually opens: approval rate by merchant, AOV, first-payment defaults, and vintage losses. Drill in, export raw data, or layer custom metrics on top.

Security

Deployment

Tech stack

Enterprise-grade

BNPL security

Certified to ISO 27001 and SOC 2, with an SDLC built around consistent security, full data encryption, role-based access, and hardened hosting for shopper and merchant data on every BNPL deployment.

Learn more

Deploy where

your team prefers

Run HES LoanBox in the cloud of your choice, on-premises, or as a hybrid setup, with AWS and Google Cloud supported out of the box.

Cloud provider

Open-source

backend foundation

Java LTS, BPMN 2.0, Camunda, and Form.io modeler form the open-source backbone of HES LoanBox. No licensing fees pile up beyond the platform source, so cost stays flat as your BNPL programme grows across markets.

Java LTS stack

HES FinTech has been our reliable technology partner since 2012. I believe much of our success is due to the well-architected HES LoanBox solution.

HES FinTech offers comprehensive front-to-back solutions with integrations. Our machine learning platform will allow clients best-in-class investment advice.

In just 6 months, we went from storing all our data in Excel to a fast, reliable, and user-friendly platform that caters to our specific needs.

HES FinTech developed our lending software and predictive analytics. Their expertise delivered automation, clear UI/UX and customer portal.

The LMS provided flexible repayment options, automated restructuring and branch-level management, enhancing efficiency and risk mitigation.

The 2026 reality of

BNPL

+15,000%

BNPL e-commerce value growth since 2014

BNPL e-commerce spending climbed from $2.2 billion in 2014 to $342 billion in 2024, per Worldpay's 10th Global Payments Report. Static rules and one-size-fits-all underwriting cannot scale into that volume cleanly.

47%

BNPL users paid late in 2026

LendingTree's 2026 BNPL Report found 47% of BNPL users paid late on a loan in the past year, up from 41% in 2025 and 34% in 2024. The trend, not the headline, is what underwriting has to price.

15 Jul 2026

BNPL under FCA in the UK

The UK begins regulating third-party BNPL on 15 July 2026, with affordability checks, FCA authorisation, and Consumer Duty obligations applying at every checkout. Manual workarounds will not survive the first supervisory review.

63%

BNPL borrowers with simultaneous loans

A CFPB study found 63% of BNPL borrowers held multiple BNPL loans at once and 33% had loans across different providers. Without bureau reporting, the stack is invisible until the first missed instalment surfaces it.

Launch BNPL

in 3 months

Bring the merchants and shoppers, HES LoanBox brings the platform.